Ask a Loan Advisor

The End of Easy Money

The End of Easy Money

The Federal Reserve (Fed) has maintained an easy money strategy since the credit crisis of 2007-2008. The Fed accomplished this by an unconventional plan of buying US Treasury bonds and mortgage securities, along with its traditional means of decreasing Fed funds rates. Initially, this strategy appeared to be an emergency plan to stabilize the financial markets immediately and prevent further deterioration of the economy amid the credit crisis. To the Fed's and the US Department of the Treasury's credit, the plan worked.

This plan was carried out for the long term until November 3, 2021, when the Fed announced a change in its policy to reduce the amount of debt from its holdings (debt regarding US Treasuries and mortgages). This shift in Fed policy is no surprise to many Fed critics. These critics know that the past Fed's easy monetary policy is a contributing factor to inflation. With the shortage of goods in various industries, we have reached the standard economic definition of inflation, which is "too much money now chasing too few goods."

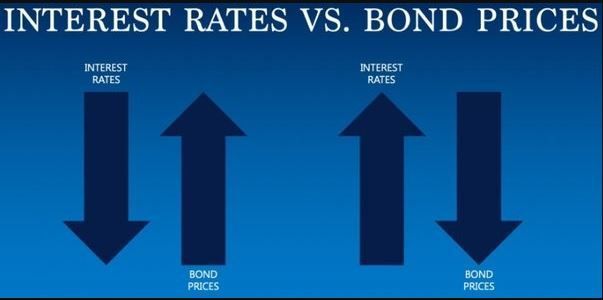

On November 10, 2021, the October consumer price index (CPI) caught the market by surprise, reporting at 6.2%. The yearly average for 2021 is now at 5.4%, which translates to inflation. At the same time, the key benchmark of long-term rates is the 10-year Treasury note yield (rate) at 1.58%. Thus, the 10-year Note appears to be yielding negative returns.

Inflation is one problem for the Treasury market and general securities (bonds and stocks). The other problem is that the Fed is dialing back on the demand factor that promoted the lower rate over the past dozens of years.

In summary, the Fed's policy change to reduce its purchases of treasuries reduces demand, and combined with negative real yields of treasuries, it is detrimental to the general debt market (bonds/mortgage) prices. To compound matters, inflation (rising prices) is more substantial than anticipated by the market. The past 13 years of an easy money policy are ending; thus, the next cycle is an uptrend for interest rates.